Ryan wrote that Manning, along with U.Va. Rector Rachel Sheridan and Vice Rector Porter Wilkinson, pressured him in June to resign by suggesting that the DOJ would take away federal funding from the university if Ryan remained in office and fought the Trump administration‘s allegations of civil rights violations.

Manning said that DOJ attorneys threatened “that if I didn’t resign, they would ‘bleed U.Va. white,'” Ryan wrote in the Nov. 14 letter.

However, the former president wrote that the DOJ’s head civil rights division attorney had publicly disavowed allegations that her department had insisted on Ryan’s resignation in a “quid pro quo” deal, in contradiction of what Manning, Sheridan and Wilkinson had told him before he gave notice June 26.

Ryan further alleged that Gov. Glenn Youngkin, the three board members and attorneys hired by the board had possibly been behind the pressure to resign, instead of the DOJ. “At the very least, we had board members who were apparently more complicit than other universities,” Ryan wrote.

But on Monday, Manning wrote that he, Sheridan and Wilkinson were motivated by “a desire to protect U.Va., its students, faculty, researchers, clinicians and patients, and not by any personal or political agenda, and certainly not by any ill will toward Jim Ryan.”

Manning added that he considers Ryan a friend and that the former president “was one of the reasons my family and I chose to make a significant gift to create the Manning Institute of Biotechnology.”

Also, Manning wrote that he agreed to speak with DOJ officials by phone “one time in June to better understand the risks to the university,” which had received seven letters from the department between April and June accusing Ryan and the university of slow-walking the dissolution of the university’s diversity, equity and inclusion initiatives.

“I held a single phone call with DOJ officials, and that call also included U.Va.’s legal counsel, including outside counsel,” Manning wrote. “After this conversation, the content of which I shared with Jim, and after further review of the aforementioned letters, it was clear to me the DOJ was prepared to suspend federal funding to U.Va. immediately if certain steps were not taken, including a change in university leadership.”

The potential loss of hundreds of millions in federal funding would “have directly jeopardized the work and livelihood of many U.Va. employees, including professors, researchers, physicians and staff,” as well as laboratories and clinics “on which patients and families depend,” Manning wrote.

Ryan’s letter, which has since prompted calls from faculty and staff groups for Sheridan and Wilkinson to resign from the board, depicts a more complex situation.

Sheridan and Wilkinson had already spoken with DOJ attorneys before the board’s early June meeting, when they presented a report to the board, Ryan wrote, although he alleged that neither woman mentioned that the DOJ had insisted on his resignation at that time. Further, Manning had in early June advised the president to “hang on” and not resign.

But Manning’s advice changed on June 16 when the two men met for lunch, Ryan wrote.

Manning “told me that he had heard from both the governor and Rachel about the need for me to resign,” Ryan wrote. “He told me that, as a friend, he did not want me to go through the ordeal of trying to fight the federal government, and he was worried what the DOJ — and other agencies — might do to U.Va., especially with respect to research funding. He also told me that I would likely be blamed for the losses. It was unclear to me whether this conversation was Paul’s idea, or whether he was carrying water for the governor and Rachel.”

Ryan also wrote that Harmeet Dhillon, assistant U.S. attorney in charge of the DOJ’s civil rights division, has “publicly and unequivocally stated — twice — that neither she nor her colleagues asked for my resignation or offered some sort of quid pro quo. That is not what Rachel, Porter and Paul conveyed to me. Who is telling the truth?”

However, Manning wrote, “Based on the information available to me at the time, I ultimately became convinced that federal funding was at risk and would result in an immediate loss of financial support to the university.

“It was, in my mind, a difficult choice between two unfortunate outcomes: real damage to the university, its people, and its academic and research mission, or the premature departure of a leader who had contributed to many successes at the university.”

According to the Virginia Athletics Foundation, which announced the gift last week, the contribution from Drew and Kate Parker will be used at the discretion of Athletics Director Carla Williams.

“This gift to the [Athletics Director’s] Excellence Fund will provide support for recruiting and operations,” Williams said in a statement. “This type of philanthropic generosity is critical in this new era of collegiate men’s basketball, and we are very grateful for Kate and Drew’s commitment to helping us.”

The Charlottesville university did say how the $5 million would be allocated and did not immediately return requests for additional details.

Although Drew Parker graduated from the University of Illinois Urbana-Champaign in 2000, U.Va. said the Parker family “believes in the power of athletics to shape character, build community and elevate U.Va. on a national stage.”

“Our mission is to develop men of character who pursue excellence on and off the court,” Ryan Odom, the head men’s basketball coach, said in a statement. “Their investment will help make that possible by ensuring our student-athletes have every opportunity to reach their full potential. We’re honored to have their support and thankful for their tremendous commitment to Virginia Basketball.”

Kevin Miller, the Virginia Athletics Foundation’s executive director and deputy athletics director, called the donation “transformational” and said the money “fuels our pursuit of excellence and gives our student-athletes the resources they deserve.”

“We are profoundly grateful to the Parkers for their visionary leadership, which not only elevates our momentum but inspires others to champion the future of our teams,” Miller said in a statement.

The foundation serves as the fundraising arm for U.Va’s 27 men’s and women’s Division I sport programs.

Carter Machinery’s roots trace back to 1928, when Robert Hill Carter founded Virginia Tractor Co., the state’s first Caterpillar dealership, in Richmond. Today, the company is an independent dealer with more than 30 locations. It has more than 2,300 employees in Virginia, West Virginia, Maryland, Delaware and Washington, D.C.

TTR Sotheby’s International Realty, the firm that sells luxury real estate to the rich and famous in the Washington, D.C., metropolitan region, started off the last month of the year with leadership changes.

On Monday, the firm announced that Mark Lowham, its longtime CEO and managing partner, has transitioned to chairman. David DeSantis and Derrick Swaak, previously co-chief operating officers at TTR Sotheby’s, will take on new leadership roles. DeSantis will become CEO, while Swaak will be president and COO.

“The strategic leadership changes at TTR Sotheby’s International Realty reinforce the strength and longevity of the Sotheby’s network when combined with high-performing local ownership,” Jonathan Taylor, who founded the firm that became TTR Sotheby’s with Wallace Tutt in 1988, said in a statement. “Mark, David and Derrick are exactly the kind of leadership team we need as the firm advances its leadership in the luxury real estate sector.”

In his new position, Lowham will focus on strategic oversight, board engagement, growth partnerships and long-term value creation.

As CEO and managing partner since 2011, Lowham is credited with leading the firm through a tenfold increase in sales volume to nearly $6 billion in annual sales, according to a news release. He’s also led agent growth and expansion to markets including Maryland’s Eastern Shore.

Lowham represented the seller of The Cliffs, a McLean home that went for $25.5 million to a mystery buyer in October 2024. He also sold his own McLean home in March for $6.15 million, down from the original listing price of $7.95 million.

“While I transition into this role, I remain deeply committed to driving value for our advisers, clients and the global Sotheby’s real estate network,” Lowham said in a statement. “I am proud to work closely with David and Derrick, confident in their ability to grow our market share while enhancing service.”

DeSantis, who became co-chief operating officer in 2023, joined TTR Sotheby’s as a partner and managing broker in 2007. He has a track record, according to the firm, of high-performance real-estate operations, agent development and using technology for growth. In his new position, DeSantis will lead day-to-day strategic execution and agent productivity initiatives while driving the firm’s growth targets.

As TTR Sotheby’s president and COO, Swaak will oversee operational discipline, process enhancements, marketing and adviser experience. He also joined TTR Sotheby’s in 2007 and became co-chief operating officer more than two years ago. In 2021, Swaak served as board president for the Northern Virginia Association of Realtors, and in 2022, he was named NVAR Realtor of the Year.

TTR Sotheby’s is an independently owned and operated affiliate of the Sotheby’s International Realty network. It has nearly 550 advisers and 13 office locations.

Starbucks to pay $38.9 million to over 15,000 NYC workers.

City says the company cut hours and denied stable schedules.

Settlement includes $3.4 million in civil penalties and reinstatement rights.

Investigation began after widespread worker complaints in 2022.

NEW YORK (AP) — Starbucks will pay about $35 million to more than 15,000 New York City workers to settle claims it denied them stable schedules and arbitrarily cut their hours, city officials announced Monday.

The company will also pay $3.4 million in civil penalties under the agreement with the city’s Department of Consumer and Worker Protection. It also agrees to comply with the city’s Fair Workweek law going forward.

A company spokeswoman said Starbucks is committed to operating responsibly and in compliance with all applicable local laws and regulations in every market where it does business, but also noted the complexities of the city’s law.

“This (law) is notoriously challenging to manage and this isn’t just a Starbucks issue, nearly every retailer in the city faces these roadblocks,” spokeswoman Jaci Anderson said.

Most of the affected employees who held hourly positions will receive $50 for each week worked from July 2021 through July 2024, the department said. Workers who experienced a violation after that may be eligible for compensation by filing a complaint with the department.

The $38.9 million settlement also guarantees employees laid off during recent store closings in the city will get the chance for reinstatement at other company locations.

The city began investigating in 2022 after receiving dozens of worker complaints against several Starbucks locations, and eventually expanded its investigation to the hundreds of stores in the city. The probe found most Starbucks employees never got regular schedules and the company routinely reduced employees’ hours by more than 15%, making it difficult for staffers to know their regular weekly earnings and plan other commitments, such as child care, education or other jobs.

The company also routinely denied workers the chance to pick up extra shifts, leaving them involuntarily in part-time status, according to the city.

The agreement with New York comes as Starbucks’ union continues a nationwide strike at dozens of locations that began last month. The number of affected stores and the strike’s impact remain in dispute by the two sides.

Adobe projects Cyber Monday spending to reach a record $14.2 billion.

Cyber Week sales show strong consumer demand despite economic uncertainty.

Mobile devices expected to account for 58% of online holiday spending.

Buy now, pay later purchases projected to surpass $1B on Cyber Monday.

NEW YORK (AP) — After four days of deal-fueled spending sprees that kicked off on Thanksgiving, shoppers shifted their focus on Cyber Monday, which is again expected to be the biggest sales day of the year for online retailers.

Walmart was promoting up to 50% off on fashion on its website among some of the deals, while online juggernaut Amazon was hoping to ply customers with discounts of up to 55%.

It’s no secret that buying things online is now a staple of many people’s everyday routines. And year after year, those purchases mount during the gift-giving holiday rush. Experts expect consumers to drive record Cyber Monday spending this year, despite wider economic uncertainty.

Adobe Analytics estimates that U.S. shoppers will spend $14.2 billion online Monday, or 6.3% more than in 2024. Spending is expected to peak between the hours of 8 p.m. and 10 p.m. local time, when Adobe expects $16 million to pass through online shopping carts every minute nationwide.

U.S. consumers already spent $11.8 billion online for Black Friday, $6.4 billion on Thanksgiving Day and another $11.8 billion over the weekend — exceeding Adobe’s forecasts. Purchases made across Cyber Week — the five major shopping days between Thanksgiving and Cyber Monday — provides a strong indication of how much shoppers are willing to spend for the holidays.

“Cyber Week is off to a strong start,” Vivek Pandya, lead analyst at Adobe Digital Insights, said. “Discounts are set to remain elevated through Cyber Monday, which we expect will remain the biggest online shopping day of the season and year.”

Pandya said he will be analyzing Adobe data capturing Cyber Monday sales to see if some of the spending momentum dissipated after a strong weekend.

Deals on electronics and apparel are expected to peak Monday at 30% and 26% off average listed prices, per Adobe’s latest estimates. But other categories will still continue to see deep discounts — including toys, which Adobe expects to reach 27% off listed prices.

Meanwhile, software company Salesforce — which tracks digital spending from a range of retailers, including grocers — estimates Cyber Monday’s online sales will total $13.4 billion in the U.S. and $53.7 billion globally.

While the amount of money going into online shopping carts is expected to reach new heights Monday, rising retail prices also may contribute to any record sales figures that materialize. Consumers may be buying fewer total items. Experts say tighter budgets are causing many to shop with more precision than in years past — such as focusing on a few “big ticket” purchases, for example, and spreading out what they buy over days of promotions in hopes of getting the most bang for their buck.

Businesses and households have watched anxiously for financial impacts from U.S. President Donald Trump‘s tariffs on foreign imports. Workers in both the public and private sectors are also struggling with anxieties over job security amid both corporate layoffs and the aftereffects of the 43-day government shutdown.

For the November-December holiday season overall, the National Retail Federation estimates that U.S. shoppers will spend more than $1 trillion for the first time this year. But the rate of growth is slowing — with an anticipated increase of 3.7% to 4.2% year over year, compared with 4.3% during last year’s holiday season.

At the same time, credit card debt and delinquencies on other short-term loans have been rising. More and more shoppers are turning to “buy now, pay later” plans, which allow them to delay payments on holiday decor, gifts and other items.

Buy now, pay later loans are expected to drive $20.2 billion in online spending this holiday season, according to Adobe, up 11% from last year. The firm predicted that buy now, pay later loans would pass a new $1 billion milestone on Cyber Monday, the vast majority involving purchases made on mobile devices.

Overall, mobile devices have become the dominant shopping platform consumers are turning to for the holidays. Adobe expects smartphones, wearable tech and other handheld electronics to account for 58% of online spending this season.

Five years ago, a majority of online purchases were made on desktops.

Shopping services powered by artificial intelligence are also expected to play a role in what consumers choose to buy. For Black Friday, Salesforce estimated that AI assistants and digital agents contributed to $14.2 billion of the total $79 billion it said was spent online worldwide.

Across the holiday season, “hot sellers” will include gaming consoles such as the Nintendo Switch 2 and toys-turned-fashion statements like Labubu Dolls, Adobe said. The analytics company anticipates the newest editions of popular consumer electronics — including the iPhone 17, Google Pixel 10 and Samsung Galaxy S25 — will also see high demand.

To many, Cyber Monday is billed as the “last call” to take advantage of the deepest discounts in the days following Thanksgiving. But its reach has grown over the years.

Cyber Monday is two decades old now, dating back to when the National Retail Federation first coined the term in 2005. Today, sales continue to bubble up throughout the week — riding on the hype that the industry has built to fuel consumer spending.

LONDON (AP) — The U.K. has secured a 0% tariff rate for all U.K. medicines exported to the U.S. for at least three years, officials said Monday, in return for the U.K. spending more on new medicines.

Under the deal, the U.S. agreed to exempt U.K.-origin pharmaceuticals, pharmaceutical ingredients, and medical technology from import taxes.

The Trump administration said in return U.K. drugs firms committed to invest more in the U.S. and create more jobs.

The U.K. government said the 0% rate on all of its pharmaceuticals exports was the lowest offered to any country. As part of the deal, it said the country’s National Health Service will spend around 25% more in new and effective treatments — the first major increase in such spending in over two decades.

Officials said that means U.K. health authorities will now be able to approve medicines that deliver significant health improvements but might have previously been declined purely on cost-effectiveness grounds, including breakthrough cancer treatments or therapies for rare diseases.

“This vital deal will ensure U.K. patients get the cutting-edge medicines they need sooner, and our world-leading UK firms keep developing the treatments that can change lives,” said Science and Technology Secretary Liz Kendall.

The Association of the British Pharmaceutical Industry said the deal was “an important step towards ensuring patients can access innovative medicines needed to improve wider NHS health outcomes.”

“It should also put the U.K. in a stronger position to attract and retain global life science investment and advanced medicinal research,” said ABPI chief executive Richard Torbett.

U.S. Health Secretary Robert F. Kennedy Jr. said the agreement “strengthens the global environment for innovative medicines and brings long-overdue balance to U.S.–U.K. pharmaceutical trade.”

AstraZeneca is among pharmaceutical giants that have cancelled or paused their investments in the U.K. in recent months. U.S. ambassador Warren Stephens recently warned said American businesses will cut future investments if “there are not changes made and fast.”

Earlier this year President Donald Trump and British Prime Minister Keir Starmer agreed on a framework for a trade pact that would slash U.S. import taxes on British cars, steel and aluminum in return for greater access to the British market for U.S. products, including beef and ethanol.

Bitcoin and companies tied to cryptocurrencies extended a nearly two-month swoon Monday, tracking with a broader market sell-off in technology companies that many see as overvalued.

Bitcoin, which soared to a record $126,210.50 on Oct. 6 according to crypto trading platform Coinbase, slid 11.8% to below $85,000. That’s a decline of about 33% in just eight weeks.

Stocks across the crypto industry tumbled, with Coinbase Global sinking 5.1% and online trading platform Robinhood Markets losing 5.2%. Bitcoin mining company Riot Platforms dropped 5.4%.

Strategy, the biggest of the so-called crypto treasury companies that raises money just to buy bitcoin, tumbled 10.3%. The company has reported holding 649,870 bitcoin. As of 11 a.m. ET Monday they were worth about $55 billion.

American Bitcoin, in which President Donald Trump‘s sons Eric Trump and Donald Trump Jr. hold a stake, fell 7.2% and is now down more than 41% since Sept. 30.

Other Trump-related crypto ventures have seen declines as well. The market value for the World Liberty Financial token, or $WLFI, has fallen to about $3.91 billion from above $6 billion in mid-September, according to coinmarketcap.com And the price of a meme coin named for President Donald Trump, $TRUMP, is $5.63 compared to around $45 just before his inauguration in January.

Analysts point to a number of factors that have led to the sell-off in bitcoin and other crypto investments, including a broad risk-off sentiment that has gripped markets this fall, sending investors toward safer havens such as bonds and gold.

Bitcoin futures are down nearly 24% in the past month. At the same time, gold futures are up almost 7%.

In a research note to clients last week, Deutsche Bank analysts also attributed the recent declines in crypto to institutional selling, other long-term holders collecting profits and a more hawkish Federal Reserve. Stalled crypto regulation has also contributed to the uncertainty, Deutsche Bank said.

“While volatility remains inherent, these conditions indicate Bitcoin’s portfolio integration is being tested, and raises questions of whether this is a temporary correction or a more prolonged adjustment,” the analysts wrote.

One popular way of investing in bitcoin is through spot bitcoin ETFs, or exchange-traded funds, which allow investors to have a stake in bitcoin without directly owning the cryptocurrency. According to data from Morningstar Direct, investors pulled $3.6 billion out of spot bitcoin ETFs in November, the largest monthly outflow since the ETFs began trading in January 2024.

Hampton’s Coliseum Central area is getting a new apartment-style hotel.

North Carolina-based stayApt Suites has announced plans to open a 103-suite hotel at 2122 Hartford Road, with an expected opening in summer 2026.

The hotel, designed for extended stays, brings new lodging to an area that hasn’t seen a hotel debut in years. The property, owned by Coliseum Central Hospitality, will add to stayAPT Suites’ growing footprint across Virginia, where the brand also operates locations in Suffolk and Alexandria.

“We’re thrilled to introduce stayApt Suites to Hampton,” said Gary DeLapp, CEO of stayAPT Suites, in a statement. “This vibrant community is the perfect fit for our apartment-style concept, offering the ideal blend of business, leisure and military travelers. Thanks to our partnership with Coliseum Central Hospitality LLC, we’re excited to bring guests a new kind of stay experience and become part of this growing community.”

According to stayApt Suites, the new location will offer the brand’s signature layout, which includes a full-size kitchen, a dedicated living room and a private bedroom. The brand says the aim is to provide space and the “comfort of home” for extended-stay guests.

Each suite measures 500 square feet, including an open concept living area with a sleeper sofa and smart TV, a full kitchen equipped with standard appliances, a private bedroom with a king bed or two queen beds, a walk-in closet, a desk and an additional smart TV. Guests will also have access to an enclosed outdoor courtyard with a built-in grill station, on-site laundry facilities and a fitness center.

The brand said the site’s proximity to Langley Air Force Base and other military installations will make the hotel a convenient option for service members, their families and government travelers.

StayApt Suites did not provide additional details and did not immediately return requests for comment.

Headquartered in Matthews, North Carolina, stayApt Suites launched its long-term lodging hotel concept in January 2020. It has opened 40 locations in the U.S., most of which are in Southern or Southeastern states.

Grew Atlantic Union into the largest regional bank headquartered in Virginia

Oversaw Sandy Spring Bank acquisition, expanding into Maryland, D.C., and North Carolina

John Asbury remembers the start of the pandemic in 2020 — the confusion, the fear and the uncertainty.

“That was probably one of the most frightening experiences, initially, of my career, as we all began to understand this is a pandemic. This is not something that we’ve seen in perhaps 100 years,” he says.

As CEO of Atlantic Union Bank and president and CEO of its holding company, Asbury also recognized that businesses were in jeopardy and that banks would be called upon for help. Ultimately, his bank marshaled its resources and backed far more Paycheck Protection Program loans per capita than many large, national banks — including for noncustomers whose banks were lagging. It was a risk, but Asbury says that expanding Atlantic Union’s services beyond its customer base helped bring in new clients.

It also showed him and his teammates what they were capable of. To handle all of the new business, associates throughout the bank volunteered to take calls about PPP loans and fill out paperwork, even Asbury, who fielded some calls at his home late in the evening. The bank eventually processed 11,000 loans worth a collective $1.7 billion in 2020.

“It was … a defining moment for this company,” Asbury says. “We did what needed to be done, which is very characteristic of who we are.”

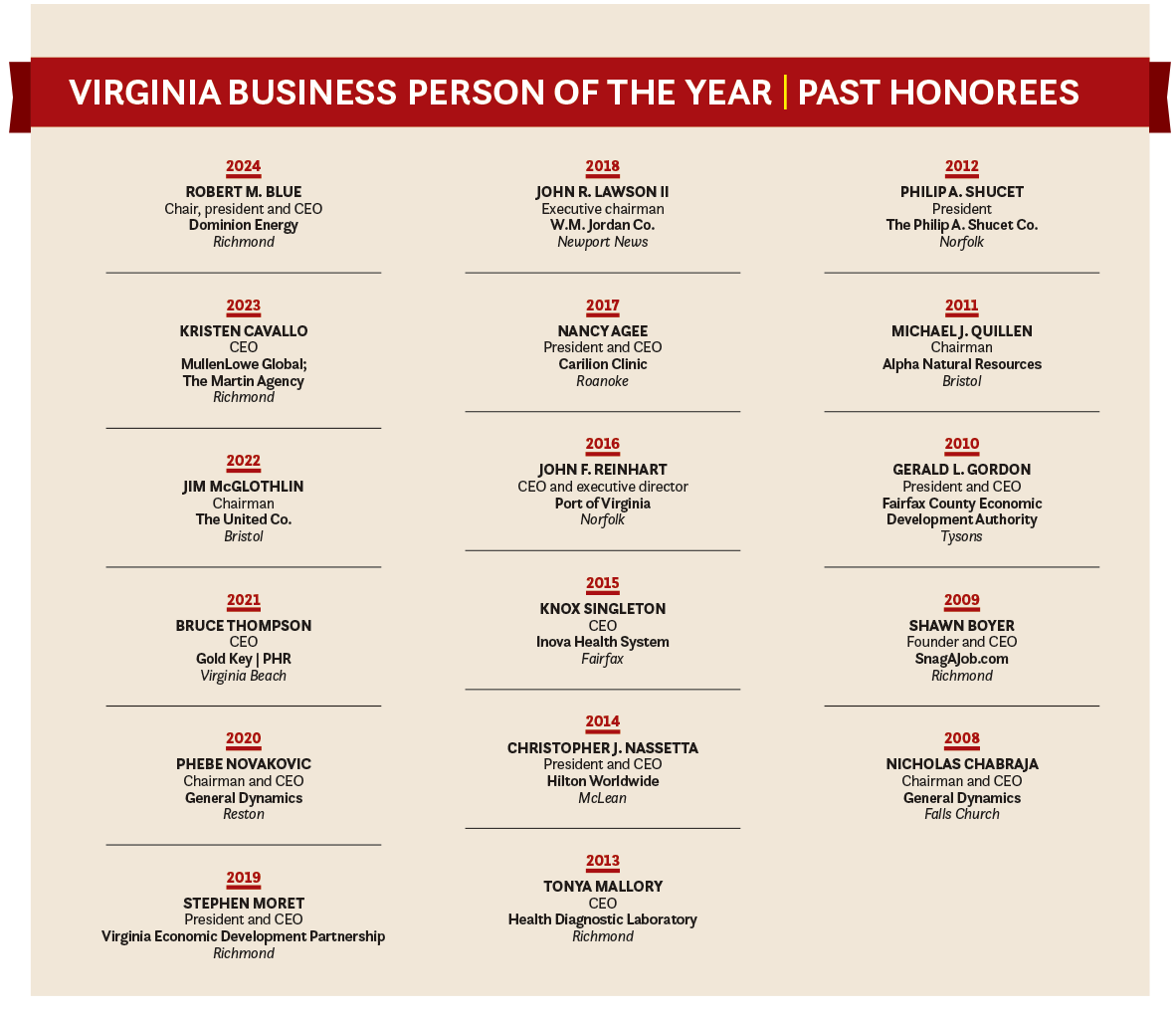

In recognition of Asbury’s nearly decadelong leadership of Atlantic Union, a period when the bank has grown from a midsize Central Virginia community bank to a regional mid-Atlantic force with presences in three states and a 6.25% market share in Virginia, Virginia Business has named Asbury its 2025 Business Person of the Year.

In 2023, Atlantic Union Bankshares transferred its listing from the Nasdaq to the New York Stock Exchange. Photo courtesy Atlantic Union Bank

Top gun dreams

Asbury self-deprecatingly describes himself as “just a guy from Radford,” even though he’s the CEO of the state’s largest regional bank. He was born in Radford and his parents met at Radford’s high school. They married and had three sons (Asbury is the middle child).

His father was a city manager in North Carolina and Tennessee, and when Asbury was an eighth grader in 1979, the family returned to Radford.

“High school was very formative to me,” he recalls, but at first Asbury was resistant to the move, “because I had my friends. I was in junior high school, which is a very delicate time period, and I came in in the eighth grade knowing no one, and I had to settle in.”

But he soon assimilated. “By my senior year, I was president of the student body,” Asbury says. “I was an honor student. I was not valedictorian. I played sports — I was good; I was not great. I received an award when we graduated, which was essentially most well-rounded. That kind of defines me; I’m good at a lot of things. I’m probably great at nothing, but I am well-rounded, and I’m interested in a lot of things.”

The other notable thing about Asbury as a teenager was his laser focus on becoming an Air Force pilot.

“I was very focused on this for as long as I can remember,” he recalls, “going back to the second grade, when I was watching the Apollo moonshot. I was fascinated with airplanes and space, and I knew what I wanted to do.”

Asbury received his appointment to attend the U.S. Air Force Academy in Colorado Springs in 1983. “My whole life plan was playing out exactly as it should,” he says.

Until it wasn’t.

By the fall of his first year at the academy, Asbury started having trouble reading the class blackboard. “What was happening is my eyes were changing,” he explains, which placed his career plans in jeopardy.

“This was a devastating experience to me at age 18. My whole life plan was disrupted. I decided toward the end of my freshman year if I was disqualified from pilot training, if I cannot be a pilot in the Air Force, I don’t want to be staff. I thought Plan B would be to join the Navy and be a naval officer, because I was interested in that too,” Asbury recalls.

“So, I came home to Virginia Tech, and I realized that I could not transfer into their corps cadets as an upperclassman. I was going to have to start over” as a freshman, he says. “I decided I’m not going to do that. So, I chose to be a civilian student.”

Asbury enrolled at Tech as a business student and also took core academic classes at New River Community College’s night school so he could graduate within four years.

“It took me quite a long time to redefine myself,” Asbury says, “and to realize I can’t control the fact that I’m not going to be a pilot, but it is what it is. I couldn’t control what happened to me. I only could control how I responded.”

At Virginia Tech, Asbury had two other life-altering experiences: meeting his future wife and working a summer job at the Radford branch of United Virginia Bank, which later became Crestar Bank.

Meeting Wendy Sublett (now Asbury) in his junior year “changed everything,” he says. “She had transferred in after two years from Virginia Western Community College, and she obviously made an impression on me. That became serious pretty quickly, and she was clear that she didn’t want to be a military spouse and, quote, move all the time.”

Asbury says culture is extremely important at Atlantic Union, influencing its workplaces and growth strategy. Photo courtesy Atlantic Union Bank

New flight plan

Meanwhile, Asbury had “stumbled across” banking as a summer job at the end of his sophomore year and had enjoyed his time at the UVB branch. He spent time learning about commercial banking and connected with David Balmer, who retired in 2003 as an executive vice president of SunTrust Banks, which purchased Crestar.

Balmer, Asbury says, “changed my life because he gave me the good advice to try to get hired by Wachovia Bank & Trust in North Carolina. It was the best training program in the South. And the original plan was [to] go down there for a few years and then we’ll hire you back in Virginia. And that’s what I did.”

Asbury joined Wachovia’s commercial banking training program, becoming a commercial credit officer, his first banking job out of college. He learned about “soundness, profitability and growth, in that order of priority,” an ethos present today at Atlantic Union, Asbury says.

“That’s how we think about our bank. The bank has to be sound, it has to be profitable. We need to grow it at a reasonable pace, not too much,” he notes. “I learned that from Wachovia.”

Along the way, Asbury earned his MBA from William & Mary and joined Bank of America, where he worked 17 years in multiple roles. This led to many corporate relocations for him and his wife.

“We probably moved, I don’t know, 14 times,” mostly with Bank of America, Asbury says. “Sadly, kids never worked for us. I’ve been married 38 years, since we graduated, and we’ve eventually concluded, all right, kids aren’t going to happen. If that’s the case, why don’t we make life an adventure?”

Asbury acknowledges that his wife, Wendy, has made sacrifices for his career, but she’s “always been supportive of me. She is my coach, she is my best friend, and I greatly appreciate her support.”

“She’s been able to do other things from a volunteerism standpoint, and she is the matriarch of the family now. I couldn’t have done this without her, and I’m in many respects a different person as a result of her. I would like to think a better person.”

Asbury progressed up the corporate ladder at Bank of America, ultimately becoming head of the bank’s Pacific Northwest region in Seattle. He then joined Regions Bank’s Fortune 500 parent company, Regions Financial, based in Birmingham, Alabama.

Although it doesn’t have branches in Virginia, Regions is one of the nation’s largest banks. After six years with Regions, where he ultimately led the bank’s business services group, Asbury says, “my wife and I concluded that we’ve done everything we wanted to do in the large bank environment.”

In 2015, Asbury made the jump to the small independent First National Bank of Santa Fe, based in New Mexico and with operations in Denver. While at Regions, he trained to become a private pilot, fulfilling his flight dream, but his new bank was not exactly wild about the idea of their new CEO flying solo, so he gave that up, Asbury notes.

However, opportunity soon knocked in Virginia.

Then known as Union Bank & Trust, the bank that would become Atlantic Union approached Asbury with an offer in 2016 to move to Richmond and become the bank’s president.

“I was not considering a change,” Asbury says. “But long story short, I was recruited. I had hit their radar. I fit the profile over there. What they were looking for [was] principally a commercial banker. I had done a lot of things during my 17 years at Bank of America and six years at Regions, and they certainly liked that I was a sitting CEO of a smaller bank, so I had exposure to that environment. And I was a native Virginian, so I suppose I checked their boxes.”

In October 2016, the Asburys arrived in Richmond.

Setting a regional course

Atlantic Union traces its roots back to Union Bank & Trust, which was founded in 1902 in Bowling Green with $2,500. By the time Asbury joined the bank in 2016, it had $8 billion in assets, with branches in the Richmond region, Fredericksburg and western Virginia. Its board was seeking a leader who could “keep the company independent and successfully cross the $10 billion asset mark,” explains Asbury, noting that regulatory costs increase dramatically for banks crossing that threshold.

Basically, he advised Union’s board, “if we want to be independent and we want to cross $10 billion, this will be a $13 [billion] or $15 billion asset bank — or it’ll simply be gone because it was too expensive.”

Asbury guided Union into its new regulatory tier, and in 2019, the bank was renamed Atlantic Union, signifying the institution’s expansion beyond Virginia’s borders. The bank has expanded further by acquiring four smaller banks under Asbury’s leadership, including its $1.3 billion purchase of Sandy Spring Bancorp in April, creating the largest regional banking franchise headquartered in the lower mid-Atlantic.

Asbury notes that Sandy Spring Bank, with more than 50 locations in the Washington, D.C., metro area, was the No. 1 regional bank based in Maryland, just as Atlantic Union is Virginia’s largest regional bank. The merger, announced in October 2024, created a bank with $38.7 billion in total assets and more than 170 branches in Virginia, Maryland, North Carolina and Washington, D.C.

Taking a page from the bank’s PPP strategy, Asbury and his second in command, Atlantic Union Bank President and Chief Operating Officer Maria Tedesco, asked employees to help take calls from Sandy Spring customers during the October systems conversion to Atlantic Union’s platform, traditionally a period with high call volume.

“We’ve had conversions that went bump in the night,” explains Tedesco, who was recruited by Asbury to join the bank as president in 2018 and has been through 30 bank conversions during her career. “But we always think about the customer first and what their experience is going to be, and we’ve gotten better at this, by the way.”

Tedesco says the Sandy Spring conversion was the smoothest in her career, and she attributes much of that success to Asbury, whom she says is “the most humble guy I have ever met,” a leader who hews to the company’s values: caring, courageous and committed.

“I have worked with so many CEOs in my time,” Tedesco notes. “I have seen it all, and I’ve had some great ones, and I’ve had some OK ones. He’s heads and tails above the rest. Why? Because he’s a transparent CEO. You’ll never, ever be surprised about anything, because he has a way of keeping people in the know.”

For 2026, Asbury says he doesn’t intend to acquire more banks and will instead focus on opening new branches in North Carolina organically.

Reaching new heights

In addition to his work at Atlantic Union, Asbury chaired the Virginia Bankers Association board in 2021, followed by serving as chairman of the Mid-Size Bank Coalition of America, and, in September, he completed his one-year term as chair of the American Banking Association, the trade organization representing the nation’s 4,500 banks. He still serves on the ABA board.

Rob Nichols, the ABA’s president and CEO, met Asbury early in his tenure at Atlantic Union and was impressed. Three years ago, Nichols approached Asbury about joining the national association’s board, as six new members must replace departing members each year.

“He’s very thoughtful, very smart, very good with people,” Nichols says. “One thing that’s very unique about him is he’s the first [ABA] chairman in 150 years who’s served at all four types of banks,” referring to Asbury’s background in large, medium, small and investment banks.

“We’ve never had that at the ABA,” says Nichols, “and he’s been absolutely fantastic.”

In 2024, the ABA and other organizations sued the Biden administration over financial regulatory policies the association asserted would hurt banks. The ABA won five out of six lawsuits, Nichols says, calling these victories “some of the most impactful actions” during Asbury’s term. Another focus was ensuring that stablecoins remain payment tools rather than vehicles for investment, which could introduce instability at small community banks, the association says.

Asbury says the Biden-era Federal Trade Commission led by Chair Lina Khan opened a “regulatory tsunami” on banks. “And while I don’t disbelieve that it was well-intended, it was overwhelming the industry and it went too far,” he says. “I believe firmly that we should have effective regulation of banking, not excessive, and I think we were being faced with excessive regulation as an industry, and the ABA was in a position to fight back, using every tool in the toolbox, including legal action.”

Along with serving on the state and national banking boards, Asbury serves on the Virginia Port Authority Commission and is now halfway through his second four-year term. Learning about the Port of Virginia’s functions and factors like tariffs and labor unions was challenging, but Asbury appreciates the experience.

“I felt at first like I was listening to a foreign language,” Asbury jokes. “I do speak the language now. I hope Virginians appreciate what a fine organization that [the Port of Virginia] is for the commonwealth, how well-run it is, and how important it is for the Virginia economy.”

Although Asbury acknowledges thinking about work outside of work, he enjoys running through Richmond neighborhoods, an activity he shared with his Italian water dog, Mozzi, who died last year.

Although Asbury and his wife miss Mozzi, “there will be another dog in our future,” he says. “Now the big debate is whether we should go puppy or rescue.”

Another benefit of living in Richmond, Asbury says, is being closer to Radford and his parents, who are now in their late 80s.

“In the end, I am a native Virginian, and I’m a proud Virginian, and that’s why I love the opportunity that we have had to bring back Virginia’s bank,” Asbury says. “We are now more than Virginia’s bank, to be clear, with respect to our markets in Maryland and North Carolina. But you know, this is where it started, right? And this is my home state.”

Launched in cooperation with the Virginia Bar Association in 2000, the Legal Elite is jointly produced by Virginia Business and Virginia Lawyers Weekly. Lawyers licensed in Virginia are asked each year to identify the top attorneys across 21 legal specialties. Additionally, up-and-coming attorneys are recognized under the Young Lawyer category.

In compiling the Legal Elite, Virginia Business contacted more than 14,000 attorneys and more than 50 law firms, directing them to a balloting website, which was available only during the annual voting period. Virginia Business contracted with Colorado-based media research and analytics firm DataJoe to conduct balloting.

This year’s Legal Elite list includes a total of 1,605 lawyers, 38.4% of the 4,179 attorneys who were nominated by their peers this year. Attorneys cast 902 ballots, making 17,363 separate votes across all legal specialty categories.

Additionally, the 18 attorneys who have appeared in all 25 editions are recognized on Page 40. Ten are from Central Virginia, while five are based in Hampton Roads and three are in Northern Virginia.

Two firms are well represented in this list of 26-year honorees, with three attorneys each. Willcox & Savage has Allan G. Donn, William M. Furr and Thomas G. Johnson Jr. Williams Mullen also has three long-term honorees: William D. Bayliss and firm president, CEO and Chairman Calvin W. “Woody” Fowler Jr., who are based in Richmond, and Thomas R. Frantz, the firm’s chairman emeritus, in Virginia Beach.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept All”, you consent to the use of ALL the cookies. However, you may visit "Cookie Settings" to provide a controlled consent.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.

Sign In

Sign In

Free Newsletter

Free Newsletter